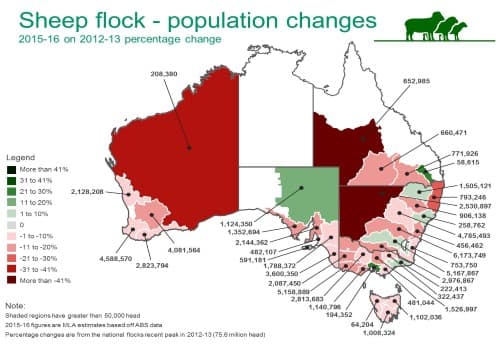

How have regional sheep populations fared since 2013?

Across Australia, regions recording growth in sheep populations since 2013 are far and few in between – with climatic challenges and shifting production systems underpinning the flock decline over the past few years.

The map below illustrates the percentage change in each region from where the sheep flock was in 2012-13, to where it was estimated to be in 2015-16 (ABS, MLA). The varying shades of green or red represent the magnitude of rises and falls, respectively, and the numbers are the estimated sheep population in each region.

Results in NSW were mixed, largely due to very patchy rainfall during the drought period, which left many producers with little choice but to destock – particularly in the western parts of the state. A transition towards or incorporating cropping enterprises, particularly among younger generation producers, has also contributed to these declines in sheep numbers across NSW. Some southern and north-eastern regions were the exceptions, with increases of up to 10% estimated in these areas.

Western regions of Victoria experienced very dry seasonal conditions during 2014-15 and 2015-16, which saw sheep numbers decline, while the shades of green around Gippsland region and the surrounds of Melbourne are likely the result of better rainfall.

The large region in north-east SA recorded 11-20% flock growth, likely fuelled by above-average rainfall in that area over the past couple of years.

The WA sheep flock has contracted across all regions from 2012-13 to 2015-16. Numbers in the highly sheep-populated areas in the south-west corner of the state declined up to 20%, while the remaining northern and eastern regions were down between 31-41%. The falling sheep population in WA is largely attributed to the shift in land use towards crop production.

While regions in south-west Queensland experienced significant drought-induced reductions in sheep numbers, there was a pocket in the south-east part of the state that registered 21-30% flock growth. Despite this area shaded green representing a relatively small proportion of Queensland’s total flock, it supports anecdotal evidence from MLA’s Lamb Forecasting Advisory Committee suggesting more producers are investing in fencing and that there is stronger interest in the sheep industry. Furthermore, the June MLA and AWI wool and sheepmeat survey results for the number of lambs on hand versus expected lamb sales in Queensland indicate that some growers may be starting to rebuild their flocks.

MLA currently estimates the national sheep flock to be 70 million head, as at June 2016. Given the wide-spread drought has broken and assuming average seasonal conditions remain, the flock is expected to continue to recover towards 73 million head by 2020.

Facebook

Facebook YouTube

YouTube Instagram

Instagram